Risks and Opportunities in the Battery Supply Chain

Key Findings

- The battery supply chain is misunderstood and undercapitalized. This will be the primary constraint to the rollout of electric vehicles.

- While there are enough mineral reserves, the mining industries ability to ramp up production and chemical refining capacity is a significant concern.

- Unlike lithium, there appear to be reserve shortages on the horizon for class one nickel and cobalt.

- China has accumulated a dominant share of ownership across the supply chain. Concentration of supply is a risk for all battery users. For governments and international organizations that have decarbonizing goals and objectives, the concentration of supply is also a risk.

- OEMs prioritize the surety of supply and quality. Several of the largest battery producers in the world (principally Chinese firms) do not currently meet the specification standards of Tier 1 western OEMs.

- I currently see limited investment opportunities in upstream lithium mining but several opportunities in lithium refining, and throughout the supply chain with nickel and cobalt.

Despite the increasing coverage of electric vehicle (EV) growth by the financial media, the metals and minerals supply chain that underpins the industry is misunderstood. Furthermore, there has been a disproportionate investment in downstream infrastructure at the expense of upstream infrastructure. The lack of investment in upstream assets will likely result in the metals supply chain constraining the near-term rollout of EVs, irrespective of consumer demand.

The changes to the transportation and energy industry over the next decade will be profound. Those who own the property rights, equity interests, and intellectual property for the inputs that feed the change will stand to accrue a significant share of both the wealth and geopolitical influence over these two critical industries. As RCS Global, a mineral supply chain consultant aptly noted, metal supply chains are complex and have significant compounding risks. The most pressing risks at the current time are opportunities for diligent investors.

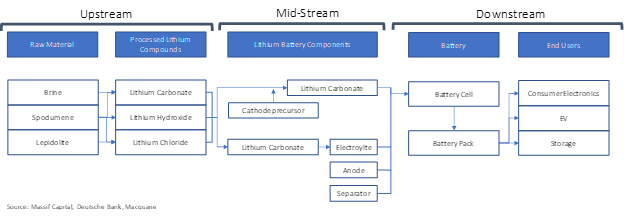

The Battery Supply Chain

Lithium-ion batteries are one of many electrochemical battery technologies. For the EV and consumer electronics industries, lithium-ion chemistries continue to be the battery of choice due to their high energy density. While lithium only constitutes roughly 2% of the battery by mass and 1% of the total battery costs, it’s the critical charge carrier of electrons within a battery and an important place to start our evaluation of supply chains.

The lithium supply chain can be split into three components: upstream, mid-stream, and downstream. Upstream companies provide lithium compounds for cathode and electrolyte manufacturing, mid-stream players produce components for batteries (the cathode, anode, and electrolyte), and the downstream segment of the industry assembles batteries and packages them together. A high-level industry supply chain looks something like the graphic below.

The most recent spike in lithium prices [1] (a 310% increase from late 2015 to late 2016) was focused on the raw material component of the supply chain. Unfortunately, this focus was short lived and ill-conceived for the simple reason that no shortage of lithium existed and many explorers and junior miners were ill-equipped to deal with the complications associated with processing lithium, in essence, incapable of bringing a discovery through development and into production. As the price of lithium returned to earth, many of these explorers have found themselves short on capital and unlikely to get their projects to a state of steady production.

For lithium, metal in the ground is not our primary concern...

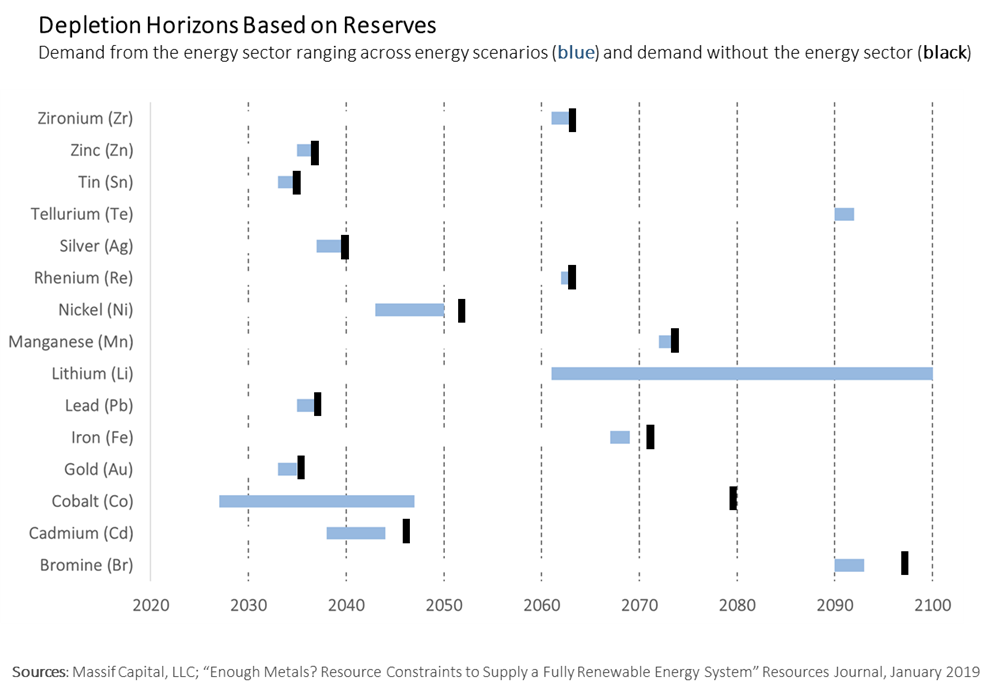

The transition to EVs and an electrical grid increasingly powered by intermittent renewable sources depends on a portfolio of energy minerals, of which lithium and cobalt are the most widely known. Other essential metals include nickel, manganese, and numerous niche metals that are usually only mined as a byproduct of mine focused on another metal. In early 2019, a team of researchers at the Laboratory of Environmental and Urban Economics in Switzerland looked at 29 metals that play an essential role in renewable energy technologies to determine whether proven mineral reserves (that which can be extracted economically today with current technology) and resources (metal for which there is a reasonable prospect of eventual economic extraction) are sufficient to support a fully renewable energy system by 2050. The report concluded that reserves of several metals appear insufficient, meaning that capital must be invested to convert known resources into reserves if the mining industry is going to meet future demand.

Estimating reserves decades into the future is an error-prone forecasting exercise. The analysis is important however as it provides context around the size of reserves today, relative to other minerals. Furthermore, it demonstrates the degree of variability in depletion rates depending on the change of quantity demanded over time.

Figure 2 below shows the range of depletion horizons for critical metals across five different energy demand scenarios. [2] The black bars represent the number of years until the reserves are depleted given current demand. Reserves of eight metals, (Cd, Co, Au, Pb, Ni, Ag, Sn, Zn) appear to have insufficient reserves (at 2018 levels) to support demand growth needed through 2050. It’s important to note that this study includes a static demand forecast for EV adoption as the principal focus was to consider varying degrees of renewable energy generation. As the EV industry will likely dominate the lithium, cobalt, graphite and nickel supply, it is reasonable to assert that the depletion rates for those four metals will be a multiple greater than depicted in the chart. The longer the depletion range (as indicated by minerals Cd, Co, and Ni), the greater the uncertainty in reserves given the varying levels of demand.

Lithium reserves appear abundant. Depletion rates with even the most aggressive demand scenarios suggest plentiful reserve capacity through 2050. It is our belief that the market is well supplied despite the fact the lithium will likely have one of the highest annual demand growth of any of the primary battery metals. This contention is supported by the fact that lithium mine supply capacity currently outstrips demand with the McKinsey Basic Materials Institute reporting in April of 2018 that the utilization rate for mine production capacity is only at approximately 50% with the utilization rates in China as low as 15%. [3]

Looking to the future, every major producer of lithium is currently engaged in either greenfield or brownfield expansion projects. Our research suggests that there are at least nine projects from known entities that are scheduled to come online between now and then end of 2021, capable of producing 312 kilotons of lithium carbonate equivalent, or 93% of the expected 2020 demand for lithium.

This does not mean there are no opportunities in lithium, only that miners are unlikely to be the highest returners. As I will discuss below, despite the abundance of raw lithium that will soon become available, raw lithium must undergo extensive chemical treatment to be used in batteries, especially in the case of lithium hydroxide from Australian spodumene deposits. As such, I believe that investors looking for opportunities in the upstream segment of the lithium industry are best off waiting for opportunities to buy lithium “majors” when they are trading at steep discounts. Not only do the majors, such as Albemarle, SQM or Livent, have well-established mines with extensive brownfield expansion opportunities, which have less capital intensity then greenfield projects, but they also have well-established refining processes in place. The importance of processing for lithium cannot be understated; lithium is not like gold, it does not come out of the ground in a state that is usable, the majors understand that lithium is a chemical business with a mining component, not a mining business.

Returning to the Laboratory of Environmental and Urban Economics report, the conclusions should be read with a wide margin of error. Importantly, I believe that efficiency gains in metal productivity, paired with an increasing ability to substitute metals economically will occur before ore grades decline. Furthermore, unlike fossil fuels which degrade through combustion, many metals retain their chemical properties after use to varying degrees and thus can be recycled. This offers a greater potential for a circular economy to develop around energy metals and will be necessary to fill deficits created through short term refining and processing bottlenecks.

To ensure that reserve quantities do not become a future problem, metal substitution [4] and recycling infrastructure [5] will be key. Despite the conclusions of the Laboratory of Environmental and Urban Economics, I do not believe that reserves will be the most pressing constraint within the battery supply chain. Instead, I think the problem lies in the expansion of production and refining capacity. The result is that I foresee the evolution of a duel bottleneck within the battery supply chain. First, there is a lack of capital flowing into mining projects to convert resources into reserves, and second, there is a lack of capital flowing into the refining for energy metals which will create significant production constraints for mid-stream producers of cathodes and subsequently upstream producers of batteries.

Unlike the well-supplied lithium market, supplies of nickel and cobalt are a concern…

The demand for metal resources has grown sharply over the last decade, particularly for energy metals used in the manufacturing of electronics and, more recently, renewable energy technologies. As EVs begin to replace the internal combustion engine, the strain on the battery metals industry will be pronounced. Indeed, within the next two years, metal and mineral demand from the EV industry will grow to twice the size of consumer electronics demand and more than 15 times the size of the stationary energy storage market. [6]

The upstream supply is currently ill-equipped to handle this explosion of growth. Since 2015, an estimated $400 billion has been committed to various stages of the electric vehicle supply chain, but only 5% has been committed to lithium and cobalt mining projects and even less to cathode production facilities. [7] With over 75% of the investment thus far coming from auto OEM’s, a significant risk exists that manufacturers will find themselves uncomfortably short of several of the essential ingredients necessary to build EVs. [8]

The capital flows into the battery ‘mega factories’ overshadows this uncomfortable fact. In 2017 there were 17 lithium-ion battery mega-factories under construction globally. Today, there are 70 under construction across 4 continents. 46 of them are in China. Since the fall of 2017, planned lithium-ion battery expansion between 2019-2028 has risen from 289 GWh to 1,549 GWh. That expansion is equivalent to roughly 23 million sedan size EVs. [9]

If every battery manufacturing facility under construction today is built and operates at 100% capacity [10], then the next ten years will see an 8x increase in demand for lithium, a 7x increase in graphite anodes, a 19x increase in nickel and a 4x increase in cobalt. [11] While many mines may have the headroom to increase production, it’s quite clear that capital will have to flow back into mining to fund the necessary expansions and exploration projects to meet the expected demand profile for many energy metals.

The cobalt and nickel supply chains face different set issues when compared to lithium. For starters, cobalt has no primary supply; it is almost always a byproduct of nickel and copper mines. [12] Furthermore, it is almost unique in the world of metals in its heavy reliance on a single supply country, the Democratic Republic of Congo (DRC) [13], a location best known for its violence, and questionable labor and mining practices. Production from outside of the DRC is also declining; the combined output from Australia, Russia, and Zambia is 28% lower than it was a decade ago. [14] Currently, the DRC is responsible for more than 60% of global cobalt supply.

Our conversations with battery procurement specialists at major consumer electronics companies and cobalt focused mining firms suggest that cobalt out of the DRC is untouchable due to potential risks associated with the conflict minerals laws and to brand reputational risks. Complicating the cobalt DRC story is the role China plays in refining. Currently, China is responsible for more than 80% of all refined cobalt. [15] According to our research, the only significant refining to occur outside China occurs at a recently sold cobalt refinery in Kokkola Finland, which refines ~17% of global cobalt. That plant was sold to Umicore for $150 million by Freeport McMoRan. [16]

China’s role in refining complicates the cobalt story because it makes many western consumers of Chinese batteries nervous about the source of the cobalt in the batteries they are buying. Unfortunately, even benign scenarios for battery growth suggest a need for cobalt production to double between now and 2025.

Returning to the mining of cobalt, because the metal is principally a byproduct of nickel and copper mining the supply is bifurcated between two other metal markets. A little less than half of the cobalt production comes from leaching of nickel-bearing laterite ores and the smelting of nickel sulfide ores. Laterite ores usually contain 1.3-2.5% nickel and 0.05-0.15% cobalt. The value of nickel is roughly 10x higher than cobalt. In other words, if the demand for nickel were to drop, it would be reasonable to expect that cobalt production would experience a reduction as well. The reverse holds true for cobalt extraction at copper mines (in some cases). For example, the Mutanda mine in the DRC produced 250 kt. of copper and 25 kt. of cobalt in 2016. Considering the copper and cobalt prices at the time, roughly 40% of the mine’s revenue came from the value of cobalt (while contributing 9% of the total by weight).

Nickel is also a concern. Class 1 nickel is required for batteries and is principally found in nickel sulfite deposits. Sulfite deposits represent a fraction of the total nickel reserves presented in Figure 2 and are distinctly different from the laterite ores, which are the type of deposits where cobalt is typically found. Considering the EV OEM push towards a NMC811 [17] cathode architecture, a 19x increase in the quantity of nickel demanded over the next decade may prove problematic. Importantly, even though roughly half of the cobalt production comes from nickel mining, the expansion of the cobalt and class 1 nickel supply chains are not synchronous because of the different deposit sources. If cobalt needs a 4x expansion over the next decade, the nickel mined with it is not necessarily fit for batteries, and it’s unclear where that additional supply will come from.

As I suggested above, although I do not foresee a lack of raw lithium, I do foresee a lack of investment necessary to bring upstream assets online for other battery metals. The dearth of investment by the mining industry, paired with the explosive growth in manufacturing requiring these inputs, suggests a problematic bottleneck in the future. One that will not be rectified quickly either, as mining remains a slow, deliberate and risky proposition.

Just because there is plenty of lithium does not mean there is plenty of marketable product….

In early 2018, Morgan Stanley issued a report calling for an additional 500 kt. of lithium supply from Chile by 2025 and a 45% drop in prices by 2021. This report has been widely cited and has contributed to the fall in equity values for companies throughout the supply chain. [18] I believe this conclusion highlights that investors are overlooking the reality that specialty lithium compounds are difficult to produce. As previously stated, lithium is not a mining business; lithium is a chemical business, with a mining component. [19]

The primary lithium market is oligopolistic with three countries, Chile, Australia, and China, accounting for 85% of global production. [20] Raw lithium concentrate is principally found in Chile, Argentina, and Australia. Refined lithium products, principally lithium carbonate, and lithium hydroxide have traditionally been mined in Chilean and Argentinean brines. Australia mines lithium from granite pegmatite orebodies that contain spodumene which until recently has been largely uneconomic given the high cost of extraction of a marketable lithium product.

The price of refined lithium has more than doubled over the last three years, turning many hard rock prospects into economically viable sources of supply. Additionally, in early 2018, SQM (the second largest lithium producer globally) resolved a long-running dispute with the Chilean government, striking an agreement to have access to six times their annual lithium production quota. Prospect miners in Australia with newfound vigor given higher lithium prices, coupled with the ‘majors’ receiving large quota expansions have contributed to the oversupply narrative in the investment community. I am not as confident.

First, missing in the detail of the SQM resolution is the somewhat onerous new royalty regime from the Chilean government that will materially lift production costs. [21] The deal is subject to renegotiation in 2030, which I believe will give SQM pause before earmarking large capital expenditures to expand capacity. Additionally, brine expansion projects are complex and costly. Albemarle’s La Negra II expansion is years behind the original projections, demonstrating the difficulty of bringing supply online, even by the experienced ‘majors.’

Supply expansion in Australia faces different challenges. Producing refined lithium from spodumene requires a range of hydrometallurgical processes, [22] and most new producers are untested in regards to processing. Despite claiming 40% of the global lithium market, Australia currently has 0% of the global lithium refining market. The infrastructure has simply not been built. Currently, much of the spodumene is sent to China for processing.

The oversupply narrative partly rests on the sheer quantity of spodumene being pulled out of the ground. The problem is that there is very little headroom in conversion capacity to take the spodumene and turn it into useful lithium hydroxide. I believe that while unprocessed stockpiles of spodumene may certainly affect the price of the raw material, it does not suggest how tight the market is for refined lithium products and specifically, battery-grade lithium. At the current time, for all the reasons above, it seems the ideal way to play future growth in lithium is to wait for opportunities to buy lithium majors, with both extensive reserves, experience and processing capabilities at steep discounts then to allocate capital to juniors. [23]

Caught Off Guard: End-Use Demand

EV market Tier 1 OEM’s have taken a back seat to the procurement of energy metals supply. To date, they have relied on the cathode manufactures to wrestle with quantity and quality of supply. It’s not clear to us that any auto manufacturer has covered its demand risk at this point. [24] Evidence of this can be seen in recent news from VW that a deal with Samsung to supply over 20-gigawatt hours of batteries was cut to around 5-gigawatt hours, not only well short of the initially proposed deal but well short of the 300-gigawatt hours of batteries some analyst believe VW will need annually. [25] It is becoming increasingly clear that battery sourcing will be a significant product bottleneck for EV manufacturers, and I expect most management teams will need to ‘adjust production expectations’ in the coming years. [26]

Quality of supply is critical for the EV revolution, and the auto industry is driving these quality requirements. I have spoken with several prominent OEM’s and consumer electronics companies. Most rank the battery production suppliers in tiers based on available quantity and quality. Tier 1 and tier 2 suppliers need to have a production capacity greater than 5 GWh. The rest are bifurcated into quality and consistency of quality. Today, only Panasonic, Samsung, and LG Chem are considered tier 1 suppliers and companies such as BYD, CATL, and SK Innovation have not yet demonstrated the requisite quality to be considered strategic tier 1 suppliers. The world will shortly have a shortage of tier 1 lithium-ion batteries, and tier 2 and 3 are not mature enough yet for western auto manufactures.

This concern is not unique to OEMs. Governments are beginning to take notice and are increasingly concerned that their stated renewable energy target objectives are heavily exposed to material and processing risk. The Netherlands just completed a review of the metal demand required for renewable electricity generation and concluded that a) future annual metal demand of the energy transition surpasses the total annual critical metal production; b) exponential growth in renewable energy production is not possible with present-day technologies and annual metal productions (ex: in 2050, the annual need for Indium, used heavily in solar panels, will exceed the current annual production 12x); c) the country is entirely dependent on countries outside of Europe, mainly China, for their critical metals; and d) their dependency risk compounds annually.

“A zero-carbon world does not do away with zero-sum games.” [27]

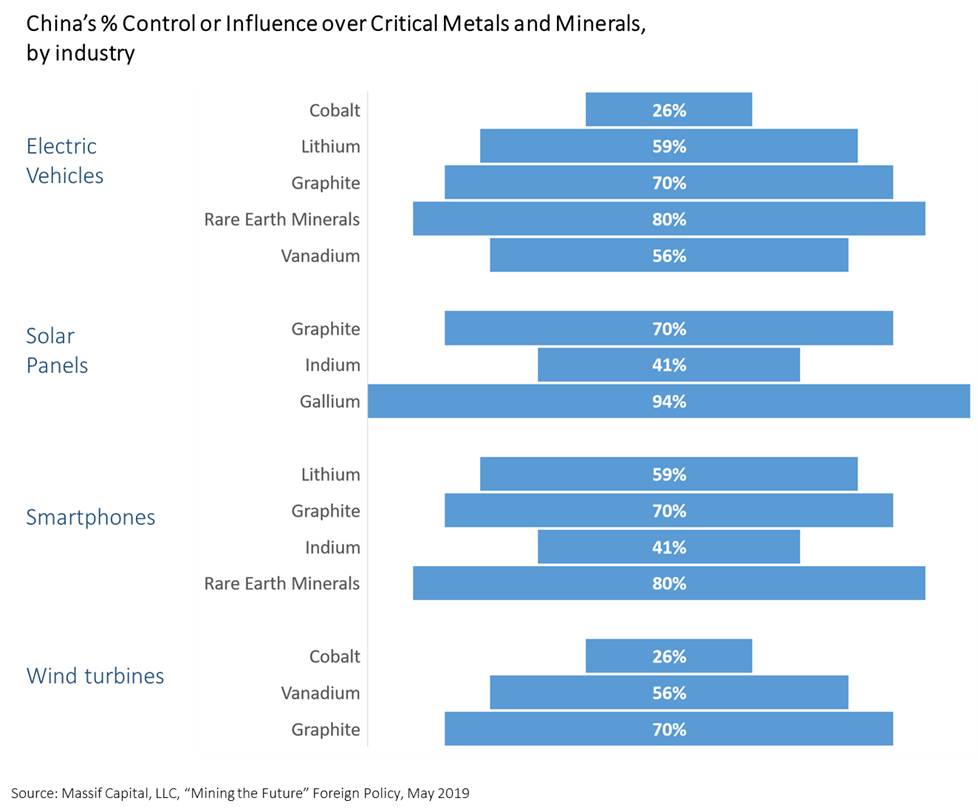

China has amassed an unprecedented concentration of market power in the energy minerals supply chain. Despite a pullback in foreign direct investment in many sectors over the last two years, China’s M&A activity in metals and chemicals hit a record high in 2018. [28] China boasts a strong resource portfolio domestically; however, they lack sufficient reserves of cobalt, platinum group metals, and lithium. Part of China’s recent foreign direct investment success has been their tolerance for political risk, enabling state-owned enterprises (SOE’s) to gain competitive advantages in complex natural resource markets. Their acquisition of cobalt resources in the DRC serves as a prime example. The state has ownership of 10 of the 18 operational mines in the DRC, six major development projects and a three-year offtake agreement with the world’s largest cobalt mine. In sum, China now owns, or has influence over, half of the DRC cobalt production. [29] In tandem with offtake agreements and equity stakes in mines, China is actively exploring in the South Africa Bushveld Complex, a rich geological formation that contains the largest reserves of platinum group metals (essential for catalytic converters) and the highest-grade deposits of vanadium. 50% of total metal exports coming out of South Africa are now destined for China.

China is also proven adept at gaining control in market-oriented, largely democratic countries. In just six years, they have gained influence or control over 59% of global lithium resources. Chemical giants Tianqi Lithium and Ganfeng Lithium are two of the three largest lithium and lithium metal producers globally.

In 2018, Tianqi acquired a 24% stake in SQM, the world’s second-largest lithium producer. [30] Led by Ganfeng, Chinese firms now have a 41% stake in all of Argentina’s planned projects, which account for 37% of their total reserves. Lithium export volumes between Argentina and China grew 4x from 2015-2017. Tianqi and Ganfeng have established stakes in 91% of lithium mining projects underway in Australia, representing close to 75% of the countries reserves. Chinese firms have deals with the developers of nine out of the eleven major lithium projects underway in Australia, two-thirds of which are exclusive.

Their reach extends beyond lithium reserves and production of refined lithium metals. China controls 70% of the world’s production of graphite and holds 24% of the known reserves. China’s Shenzhen BTR New Energy Material holds roughly 70% of global anode production. Hitachi Chemical in Japan is next in line with just 20%. [31] China accounts for 100% of the worlds uncoated spherical graphite supply, which is the processed anode material used in batteries. Figure 4 below demonstrates the scale and reach China has amassed in critical minerals.

Outside of China, there is little evidence of governments developing explicit resource strategies. Recently, US Senator Lisa Murkowski introduces bipartisan legislation (American Mineral Security Act) to “secure our mineral resources and supply chains for the country’s 21st-century auto and energy industries.” It may sound grandiose, but the Senator is correct to point out that the US is currently a bystander in what can be thought of as an arms race to hold the balance of industrial power in the energy and automotive industries. In 2018, the U.S. had a 92% import dependency on lithium, 100% import dependence on cobalt, 59% dependence on nickel, and 100% on graphite. A 2016 Government Accountability Office Report estimated that it could take the US 15 years to rebuild a domestic rare earth supply chain. [32], [33]

Compounding Risk Environment

The metals supply chain supporting the EV and renewable energy technology industries are not balanced. Committed capital expenditures by OEMs and battery manufacturing facilities are far outpacing the production and refining capacity of raw material that this necessary to feed those facilities. While there are enough mineral reserves, I am concerned about the mining industries ability to ramp up production fast enough and even more concerned about the lack of refining capacity. Furthermore, industry concentration suggests that execution risk is highly dependent on a small number of companies.

The growing divide between the demand required to scale and the current capability of the industry to produce battery-grade chemicals at scale is causing a number of companies to be mispriced. Coupled with demand expectations, this represents opportunities for investors to compound their capital. The turnover of electric vehicles is not a transitory growth opportunity. It’s a paradigm shift. Companies will be required to grow and scale at a multiple of their size today.

This transition also carries important geopolitical implications. The concentration of supply is a risk to a business. For governments and international organizations that have cooperative goals and objectives, the concentration of supply is also a risk. Today, China is investing ahead of the curve and has a commanding position throughout the supply chain. While the current opacity and mispricing of the industry look fruitful to investors, concertation risk residing in China may give many some pause. From our vantage point, a healthy diversification of countries participating in the supply chain, along with the necessary injection of capital, will be important benchmarks to the gradual maturing of the industry.

Some Extra Info (Appendix)

The Lithium-Ion Battery

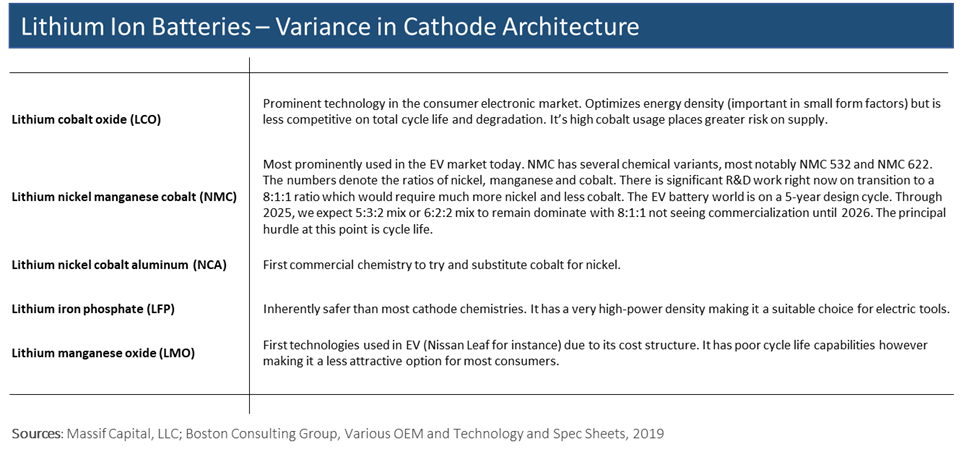

A lithium-ion battery cell has three major parts: the anode (typically graphite), the cathode (a blend of chemistries) and the electrolyte which is comprised of lithium salts. For most batteries, the difference in metals utilized, the ratio of metals, and the underlying performance characteristics of the battery, can all be found in the cathode. [34] Lithium ions are used as the charge carriers between the anode and cathode.

The figure below looks at five different lithium-ion batteries. NMC is the most popular chemical variety of the EV market today with LCO controlling the consumer electronics market. [35] It is Important to recognize that the chemical variation is an exercise of tradeoffs between varying degrees of energy, safety, life span, and cost. There is no one chemical variant that is superior to another. Batteries are fit for purpose.

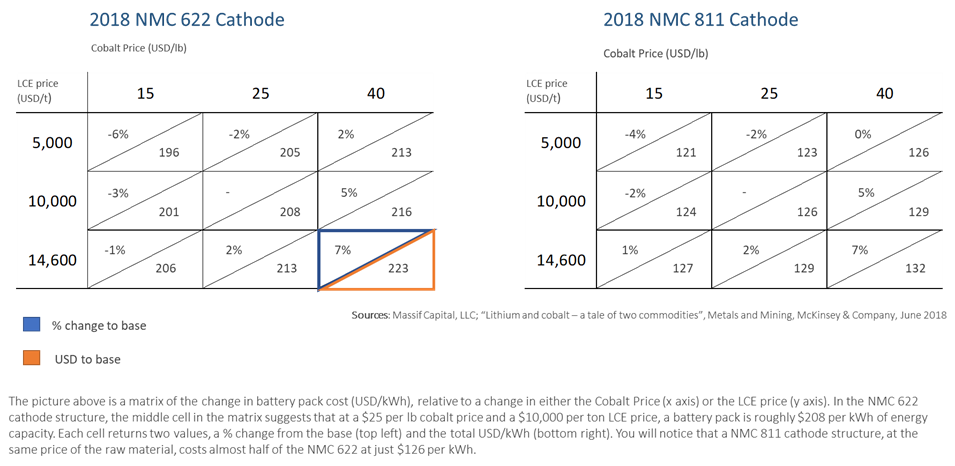

The cathode accounts for roughly 25% [36] of the total battery cost. The economics of batteries is heavily influenced by the choice of raw materials in the cathode. The figure below shows how sensitive the total battery cost is to changes in the price of lithium and cobalt.

There are two important takeaways. First, battery economics are generally more sensitive to cobalt prices than lithium prices; and second, increases in either lithium or cobalt only increase the total battery cost, and thus the total vehicle cost, marginally. It’s the availability and quality of the mineral resource that may slow EV growth, not the resulting increase in price that may soften demand.

Mining Industry : Asset Lite

The lack of capital flowing into upstream mineral production is not confined to just energy metals; it is common across a range of specialty and industrial metals. Total asset growth in mining has been in secular decline since 2008. Between 1998 and 2008, publicly traded mining firms grew assets, on average, 23% per year. The subsequent ten years from 2009 to 2018, asset growth fell in half to just over 10% a year. The last five years have been particularly bleak. Since 2014, the mining industry has grown its asset base by just 0.4% per year. [37] Beginning in 2013, the ratio of a firms CAPEX to depreciation and amortization (a rough heuristic to measure growth CAPEX vs. maintenance CAPEX) fell in half. In 2016 it went negative.

[1] Measured in USD per ton of lithium carbonate equivalent (LCE). Prices since 2010 hovered around $5,000-$6,000 per ton until late 2015 with a move towards $26,650 within a 12-month period.

[2] Two well-established scenarios attempt to estimate global energy demand exclusively on renewables: IPCC scenario and one that results from the work of Ecofys and WWF. Three scenarios from the IEA and IRENA are also included. To provide context, total global energy demand for the IPCC scenario is roughly 425 EJ/year, comprised principally of solar, wind and bio-energy.

[3] “Metal mining constraints on the electric mobility horizon”, McKinsey Basic Materials Institute, April 2018.

[4] For instance, silver can be replaced by cooper in crystalline silicon solar cells, but efficiency drops. Asynchronous motors (for wind turbines) with permanent magnets exist but are fell less efficient. Recently the switch to a higher nickel lithium ion battery away from a cobalt concentrate (in R&D and likely 5 years out) is a prime example.

[5] For most minor metals, recycling rates are well below 1%. Absent recycling, the industry will be completely reliant on mining for its raw material supply.

[6] As discussed in Part 1, non-lithium variants may come to control the stationary storage market, but lithium technologies continue to be the primary chemical catalyst in batteries for both the EV and the consumer electronics market.

[7] Benchmark Mineral Intelligence.

[8] For a deeper look into the lack of investment flowing into upstream mining, please see the Appendix.

[9] Written Testimony of Simon Moores to the US Senate Committee on Energy and Natural Resources Committee, February 2019.

[10] I recognize this is not a likely scenario but provides a useful ‘upper limit’. A strong case can be made that this is indeed still conservative as I do not include any future manufacturing expansion. If the period between 2017 and 2018 is indicative of the pace of growth, our estimate is far too low.

[11] The cobalt and nickel projections include the gradual transition from NMC532 to NMC811.

[12] This is distinctly different than lithium where more than 95% of the lithium supply comes from a lithium focused mine.

[13] Tier 1 OEMs are rightly concerned about the political risk associated with the DRC.

[14] Cobalt: Solving for a Supply Constrained Market, BMO Capital Markets

[15] Cobalt: Solving for a Supply Constrained Market, BMO Capital Markets

[16] Freeport-McMoRan Announces Agreement to Sell Portion of Cobalt Business, FCX Press Release, May 2019

[17] For additional details on varying lithium cathode architectures, please see Appendix.

[18] All else equal, a 45% drop in prices greatly impacts a firm’s revenue potential and thus its enterprise value.

[19] An excellent phrase borrowed from Joe Lowry during recent presentations in Perth Australia, May 2019.

[20] McKinsey: “Lithium and cobalt – a tale of two commodities” Metals and Mining, June 2018

[21] Indeed, as of late May 2019, SQM has already lowered production expansion expectations, citing both royalties and volatile prices.

[22] Ore is crushed and heated in a kiln to create concentrate which is then cooled and milled into fine power. Sulfuric acid is added before magnesium and calcium are precipitated out. Finally, soda ash and lithium carbonate are crystallized, heated, filtered and dried creating 99% lithium carbonate.

[23] It is probably best to stay away from Australian hard rock miners or juniors that are developing resources but lack a background/understanding in the additional complication associated with producing a marketable product from raw lithium.

[24] Meaning, based on expected new vehicle rollout, they do not have long term supply contracts to manufacture those vehicles.

[25] VW to Rework $56 Billion Battery Push on Samsung Deal Risk, Blomberg May 2019

[26] The pace of penetration will be impacted by regulations, costs and EV infrastructure. Battery costs have fallen from roughly $1,000/kWh to $230/kWh between 2010 and 2018. Some battery costs today are believed to be ~$150/kWh. The tipping point for EV’s to be cheaper than ICE cars is roughly when they cross the $100/kWh threshold.

[27] Andreas Goldthau, University of London, May 2019

[28] PwC M&A 2018 Mid-Year Review and Outlook

[29] “Mining the Future”, Foreign Policy, May 2019

[30] Of the $4.1 billion bid on SQM shares, $3.5 billion was financed by CITIC Bank International. The parent company CITIC groups is one of China’s largest state-owned financial conglomerates.

[31] Japan is also currently 90% reliant on China for its graphite.

[32] “Rare Earth Materials: Developing a Comprehensive Approach Could Help DoD Better Manage National Security Risks in the Supply Chain”.

[33] This extends beyond the mineral materials required for technologies that capture and store energy. US and NATO weapon systems are rare-earth metal dependence. Satellites are dependent on many of the same raw material ingredients. According to a July 2014 DoD Inspector General report, the Pentagon is currently not capable of properly monitoring rare earth inputs at the component or subcontractor level. Furthermore, there is no differentiation between rare earth oxides (that have no defense applications) and the post oxide materials needed for defense systems.

[34] The cathode is the positive electrode and the anode is the negative electrode.

[35] In the EV market, R&D efforts today are focused on changing the ratio of nickel, manganese and cobalt to optimize not only the performance characteristics of the battery, but to reduce supply chain risk, principally away from cobalt. On the anode side, efforts are being made to replace graphite with silicon which can increase energy density dramatically. Silicon however expands under heat and so the form factor (either in a car or cell phone/computer) becomes a concern.

[36] McKinsey: “Lithium and cobalt – a tale of two commodities” Metals and Mining, June 2018

[37] Market weighted averages. Analysis from Massif Capital. Data attributed to Thomson Reuters.