Tempering Expectations

Headlines are awash with optimistic growth projections for the energy storage market. Bloomberg New Energy Finance estimates $600 billion will be invested in the sector over the next 20 years, resulting in installed energy storage capacity growth of 1,000 GW and a 52% drop in the upfront cost of storage. Many current forecasts suggest that by 2040, storage will represent ~10% of total installed power capacity globally. The positive narrative has been buoyantly kept aloft with headlines such as:

“storage market will triple this year” (Reuters)

“big batteries are taking a bit out of the power market” (WSJ)

“price drop of 80% over 2010-17” (Financial Times)

Although I share the pundit’s optimism, principally because there is strong empirical evidence to suggest that renewable energy cannot exceed more than ~1/3rd of an electrical systems generation without putting the reliability of the entire system in question [1], I think caution is necessary. The energy storage market remains opaque and young, with a significant number of unresolved issues. Not the least of which is a common language and understanding amongst the investing public of the diversity and complication of the business.

The industry is young enough that people can still refer to it as the “energy storage industry”, even though the phrase lumps together 15+ different technologies with vastly different operating characteristics and costs. Similarly, when someone refers to the “energy storage market”, they are lumping together completely disparate markets. The appropriate comparable would be discussing the addressable market for the internal combustion engine, which would of course include everything from SUV’s and sports cars to trucks and farm equipment. Each of which is its own business, with its own technologies, and cycles. For an investor who is interested in the “energy storage market” it’s not just helpful to get more specific, its critical.

The following commentary looks at a few key topics that a savvy investor must focus on when evaluating the energy storage potential, and technologies, for the global utility market. This paper will not focus on the electric vehicle (EV) or consumer product market. Part II in this series will examine the global supply chain for batteries which is heavily influenced by the EV and consumer product market demand.

The First Key Distinction – Power, Energy & End-Use Applications

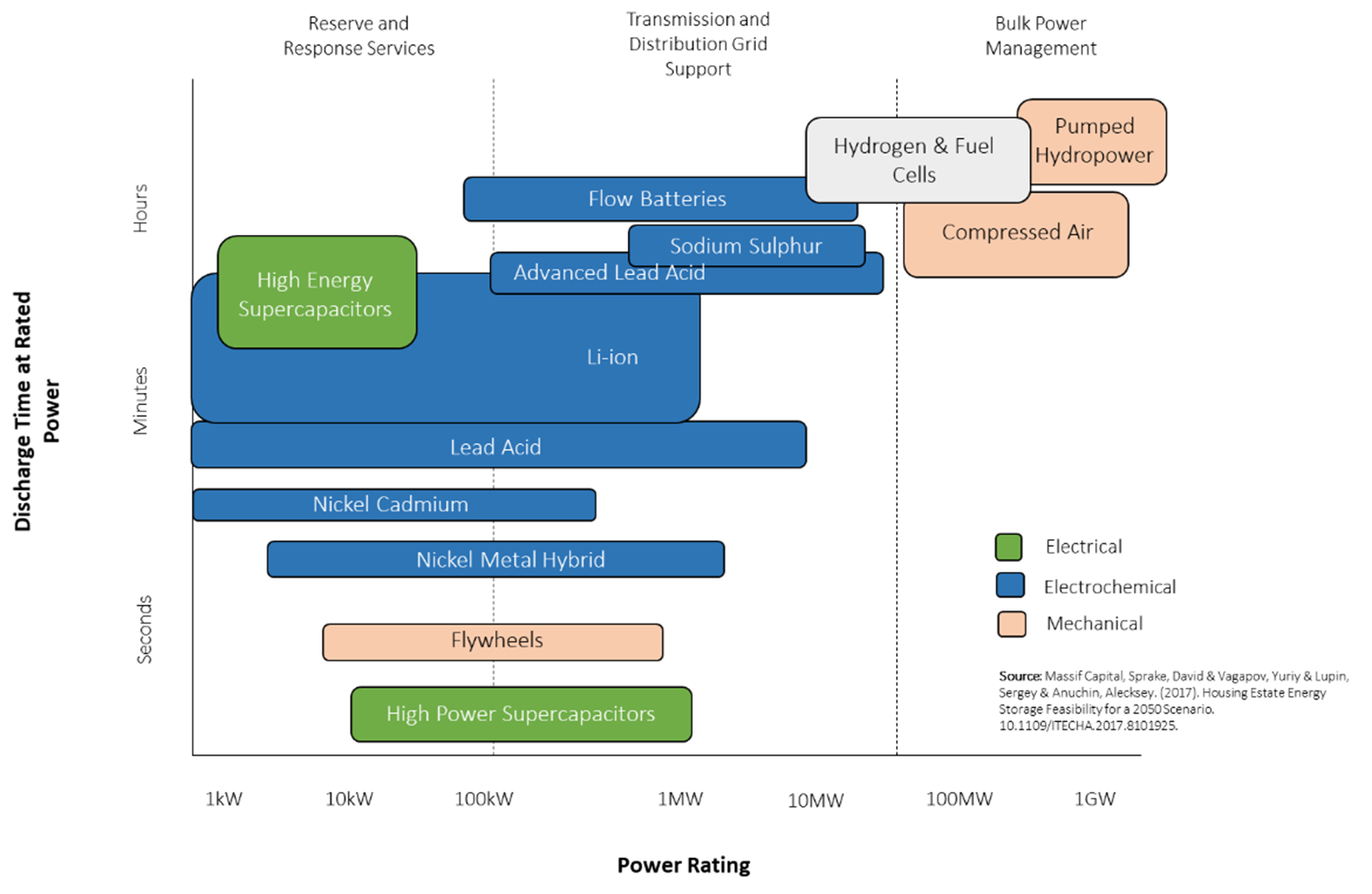

Every energy storage system has a power rating and energy rating. Power is the rate at which work is done and energy is the capacity to do work. Energy is, in essence, the amount of power expended over time. Unlike a natural gas or nuclear power plant, which only have power or capacity ratings, battery systems are designed to maximize either a power rating or an energy rating, depending on their intended use. Different end-use applications require different balances of energy vs. power. The chemical composition of batteries will often dictate whether a battery is better suited to provide a lot of power in a short amount of time or less power over a longer period.

The graphic above captures the strengths and limitations of different storage mediums in relation to the power and energy needs of an application. It’s an imperfect illustration, but it’s important to recognize that a Li-ion battery, as an example, is chemically optimized for high power output and lower energy in relation to say a flow battery which is designed for lower power output relative to energy. Finally, as the far-right side of the graph highlights, the majority of utility scale energy storage today is supplied by mechanical storage, pumped hydropower specifically. Electrochemical storage (a battery) is just a component of a boarder eco-system of storage technologies. To forget about supercapacitors and fuel cells is also mistake. While they may be further behind in technological development, their characteristics, if successfully implemented, may take over a dominate portion of the utility storage market.

Second Key Distinction - Maturity

The reason Li-ion dominates the market and headlines today is because it is one of the only mature technologies available. [2] The demand for energy storage is currently driven by problems that are solved by Li-ion batteries in a reasonable way, electric vehicles for example, and these types of storage uses will likely continue to dominate the end-use application for all energy storage for some time. Developers and capital providers looking to deploy large scale energy storage for uses other then EVs and consumer electronics, have few options to turn to when looking for a proven, bankable, solutions.

The promise of energy storage is far greater then cars and cell phones though, and frankly the promise of renewable energy in general is quickly approaching a point at which it can only be fulfilled if the additional potentiality of energy storage is met.

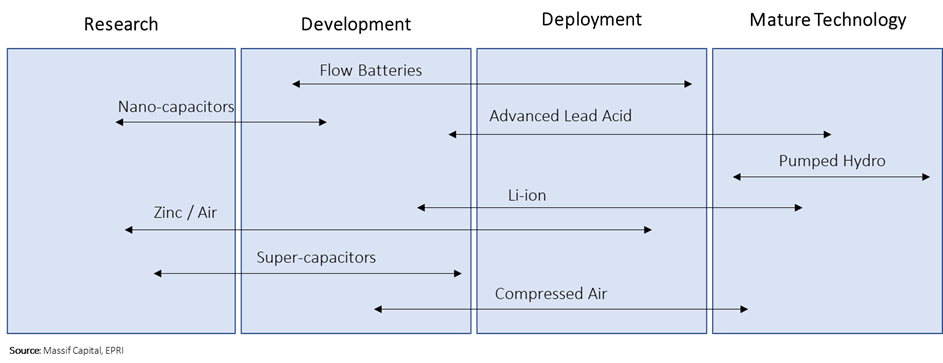

The focus on Li-Ion should be a concern and interest for investors because capital is flowing somewhat indiscriminately into Li-ion, supported by evangelists such as Elon Musk who have created a common knowledge narrative around Li-ion the solution to our storage problems. Unfortunately, as Jesse Jenkins of MIT points out, if all you had was renewable energy and Li-ion batteries such as the Tesla Powerwall 2.0, you would need 37.8 billion of them, or enough power walls standing next to each other to circle the earth 1085 times. As already discussed different applications demand different storage mediums and there exist a whole portfolio of storage technologies in different stages of maturity in need of capital. The chart below highlights just a few, with the current stage of development suggestive of the type of capital needed, be it venture capital to project finance.

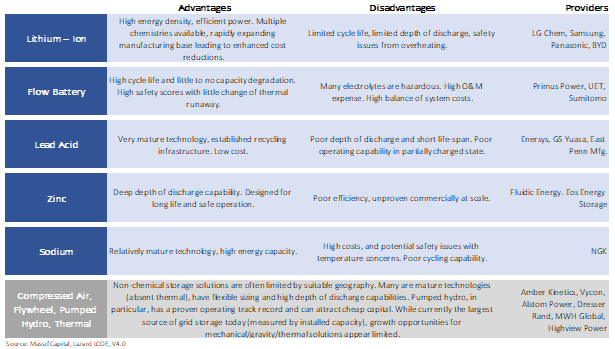

Many battery chemistries are making their way through development and small test deployments, but most do not have the installed capacity base to be considered mature. Lead acid is the only other electrochemical solution besides Li-ion that is a mature technology today; however, it has a very short cycle life. If cycled daily (one charge and one discharge), the average life of the lead acid battery is typically no more than 5 years, before the capacity and efficiency degradation render the product useless. If a developer is looking to sign a 20-year power purchase agreement, they could certainly consider the low cost of lead acid however they would need to replace the system four times over that twenty-year period, drastically increasing its levelized cost of energy over the project life.

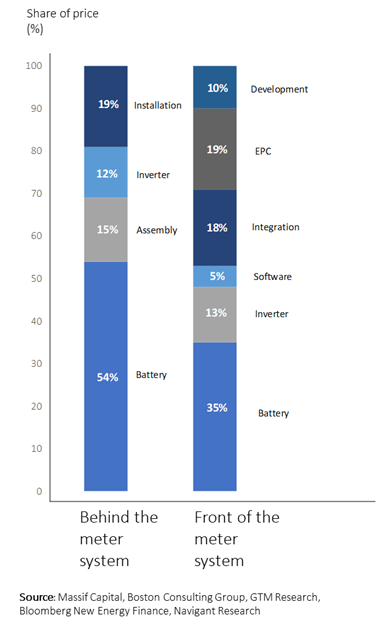

Third Key Distinction: System Costs Vs. Battery Costs

This may seem obvious, but it’s an important point. For stationary utility storage (let’s say a big battery at a substation that helps curtail peak power and defers transmission infrastructure upgrades), the cost of the battery is only about 1/3 of the total project cost. When market projections call for a “drop in price”, are they referring to total system costs or the battery costs? When doing due diligence on an investment opportunity and mapping out a technology roadmap from a vendor, the cost of batteries are often only a portion of an installed system, as the chart to the left depicts. Battery costs may fall by 50%, but do you think engineering, procurement and construction can fall by 50%? We doubt it. This is important because the size of the market is predicated on whether the total system costs of a project are in the money, not whether the battery costs are in the money.

Fourth Key Distinction: Market development vs. Technology Development

Market rules in electricity markets are currently organized around legacy assets. This limits storage from selling their potential services, reducing possible revenue streams.

In the United States, for example, an asset is either bid into a competitive auction where it can earn money on energy sold, or a regulated utility owns it and pays for it through their retail customer base. Auction rules are set by regulators (both at the state and federal level). Electricity rates (which are both how a utility makes money and the primary driver for whether a residential system is profitably) are set at the state level. Its highly regulated. A battery is not a generator – at a technical level it has obvious distinctions from 99% of the products that the current de-regulated US market has been built for. Until 2018, there were no official Federal policies in place that instructed the system operators to allow energy storage resources to participate in wholesale markets. Absent market redesign that allows for cost recovery of the asset, it is difficult to justify the economic value add of new project installation in certain markets. Market rules will change this year, which means the opportunity for storage to make money will change this year. Thus far, all independent system operators, except for California (CAISO) are behind schedule in reworking rules to be in compliance with federal regulations. Most have until the end of December 2019 to remedy that. Given these changes, market development is a far more important story in 2019 than any technologic advancement or cost reduction in the asset.

The story holds true on the retail side of the equation as well.

A small subset of retail customers may choose to purchase an energy storage system as a luxury good. Perhaps they view it as a form of reliability and independence from the utility. Most however will need to be convinced that the high upfront cost will lower their current utility bill enough such that the asset pays for itself over time. That math is dependent on retail electricity rates which is, in simple terms, a function of the cost the utility bears to build the generation, transmission and distribution assets that supply that power.

Here in lies the issue. For storage to be economic at the retail level today, retail electricity rates need to be higher. California, which has the highest electricity rates in the country, also has the highest level of retail storage penetration. California has the highest electricity rates in the country, in part because their overall system costs have become exceedingly expensive as the amount of intermittent renewable energy increases and utility programs have been required to implement costly programs to subside the proliferation of such asset. They are, in effect, creating a problem to solve.

Let us be clear: the broader transition to a low-carbon economy is a very worthwhile endeavor, and we fully support systems decreasing their reliance on thermal generation and increasing their reliance on renewable generation. That said, storage is a necessary and economic solution to a future electric grid, not our current electric grid. There are pockets of economic viability in the system today, but it is primarily helping the system become more efficient. Widespread adoption will not occur in such an environment.

Pundits will argue that storage will follow a similar path of growth that solar has enjoyed over the last decade. We believe that is a short-sided argument. As solar costs fell, it become increasingly more competitive to bid into wholesale markets. Markets had no trouble absorbing this new asset, as solar produces electricity, which is not foreign. It does not matter what the fuel source is, be it coal, gas, uranium or solar radiation. The lowest cost generation is usually able to supply that electricity. Storage is fundamentally a different product. When system operators dispatch a system, the decision making is not merely a function of economics, but also physics. It’s optimizing the lowest cost subject to the physical constraints of the grid. Storage changes the physical make-up of the electrical grid and market rules have not been written to account for that.

There’s value in energy storage, but right now very few people, or systems, want to pay for it. Our belief is that that paradigm will change, but it will lag the technological development of the chemistry and more closely align with the market rules, incentives and price signals that allow for profitable deployment.

Distinction Six: Installed project price points vs. Proposed project price points.

The last few years have brought several announcements of record low price points for solar plus storage systems.

- Xcel Energy in Colorado, with an open bid to replace 650 MW of power, received developer proposals for a solar plus storage assets at $36 per MWh, a roughly $6-7 premium to existing solar. The revenue stream, or system benefit, of a more dispatchable asset is worth easily more than the incremental $6-7 figure. However, there is no installed battery in the world today that has proven a levelized cost of energy of $6-7 per MWh (or 6-7 cents per kWh).

- In 2017, Tucson Electric Power signed an agreement to purchase a combined system by NextEra for an all-in cost less than $45 per MWh over twenty years, a figure that again, would require a sub ten cent per kWh full installed storage system.

Developers often do not have storage vendors secured when submitting proposals and are banking on technology development to fill the gap in the interviewing years prior to estimated installation date. It’s exciting to recognize the solar plus storage systems are now, theoretically, cheaper than nuclear, coal and approaching combined cycle natural gas plants; however, enthusiasm needs to be controlled until those projects are actually operating. Any inflection point that this market may see, will almost certainly come after large scale systems have been operating for several years. Investors will need to get comfortable with taking storage risk – flashy headlines may juice stock prices in the short run, but investable companies in the battery space will only come after the fundamentals are proven.

Distinction Seven: Be wary of extrapolating current technology trends

EV’s are currently driving the battery market and will continue to do so, regardless of the pace of utility stationary storage adoption. As such, the battery manufacturing and supply chain infrastructure, which influences the chemical flavor of products in the utility industry, is driven by an entirely sperate automotive industry. Many product (Apple/Microsoft) and car (Ford/GM) are forcing battery manufactures (Samsung) to lay out detailed risk mitigation plans as it relates to materials such as Cobalt. Many are looking to diversify away from using cobalt entirely in the battery, focusing on lithium iron phosphate (LFP), lithium manganese oxide and lithium titanate. LFP is the most popular of the three and may begin to control a greater share of the Li-ion market. Be cognizant of the drivers that impact the supply chain and don’t assume that demand for materials today will scale 1:1 with forecasts for estimated market size.

[1] More specifically, a reliable electricity grid cannot absorb large increases in intermittent generation without ample storage capacity. Regardless of the cost of the intermittent resource, at some point total system costs begin to increase to handle fluctuating generation in a system that is dispatched to ensure reliability.

[2] While other technologies may technically be commercially available, the amount of system data in installed projects is far behind that of Li-ion. As such, the cost of credit or the cost of a warranty is typically much more expensive for non-Li-ion technologies to ensure ample capacity is met over the course of the project’s life.